Does Renters Insurance Cover Storage Units?

We will search the top carriers for you for the best offer.

Does Renters Insurance Cover Storage Units? A Detailed Guide

Yes, renters insurance covers personal property in storage units, but with strict limits. Most policies cover up to 10% of your personal property coverage or $1,000, whichever is higher. Some states have different rules.

This guide explains exactly what is covered, what is not, coverage limits by state, and when you need to buy additional storage unit insurance.

QUICK ANSWER

Does renters insurance cover storage units? Yes, but with limitations:

- Coverage limit: 10% of personal property coverage or $1,000 (whichever is higher)

- California, New York, Connecticut, Virginia, Florida: 10% rule applies

- Other states: $1,000 maximum coverage

- Covered perils: Fire, theft, vandalism, water damage from burst pipes

- Not covered: Floods, earthquakes, mold, mildew, pest damage

👉 If your stored items are worth more than $5,000, you likely need additional coverage.

HOW MUCH DOES RENTERS INSURANCE COVER IN STORAGE UNITS

Standard renters insurance includes off-premises coverage that extends to storage units. However, this coverage is limited compared to belongings inside your rental home.

The 10 Percent Rule

Most renters insurance policies limit storage unit coverage to 10% of your total personal property coverage (Coverage C) or $1,000, whichever is greater.

Examples:

- $50,000 policy → $5,000 storage coverage

- $30,000 policy → $3,000 storage coverage

- $10,000 policy → $1,000 storage coverage

State-Specific Coverage Limits

California, New York, Connecticut, Virginia, Florida

- Coverage: 10% of personal property limit or $1,000

- Example: $50,000 policy → $5,000 storage coverage

All Other States

- Coverage: $1,000 maximum regardless of policy size

- Example: $100,000 policy → still capped at $1,000

👉 Texas average renters insurance cost: ~$20/month, same 10% or $1,000 rule applies.

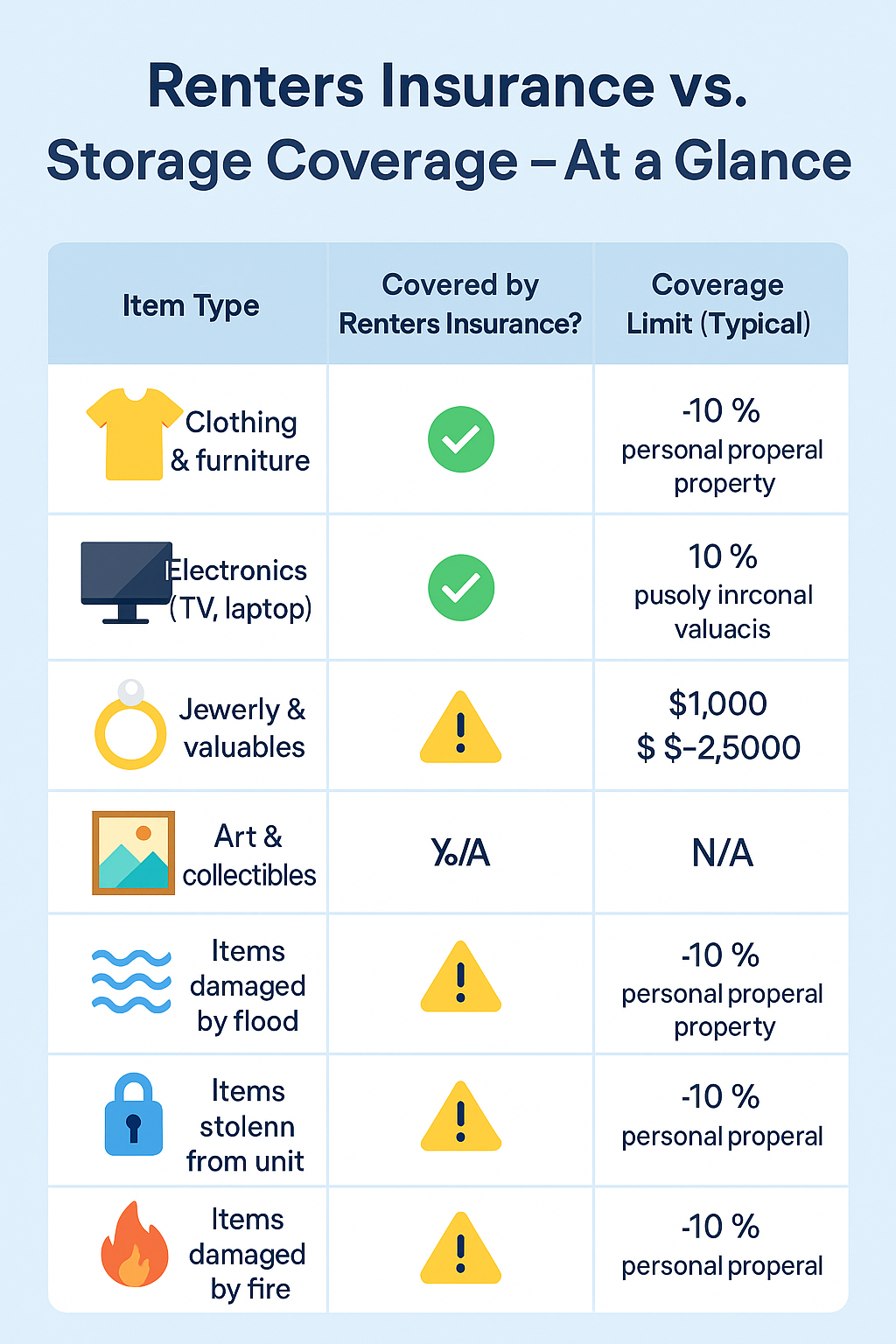

WHAT IS COVERED IN STORAGE UNITS

Renters insurance covers stored belongings against the same perils as items in your home:

- Fire and Smoke Damage – Most common risk

- Theft and Burglary – Requires police report

- Water Damage from Burst Pipes – Covered (not floods)

- Vandalism – Intentional damage covered

- Windstorm and Hail – Weather-related damage

- Lightning and Explosion – Electrical or facility incidents

- Impact by Vehicle – If vehicle damages the unit

WHAT IS NOT COVERED IN STORAGE UNITS

- Flooding – Requires separate flood insurance

- Earthquakes – Not covered without endorsement

- Mold and Mildew – Considered preventable

- Pest and Rodent Damage – Excluded

- Normal Wear and Tear – Not covered

- Vehicles in Storage – Require auto insurance

COVERAGE LIMITS FOR VALUABLES

Even within your limit, sub-limits apply:

- Jewelry: $1,500

- Cash: $200

- Coins/Collectibles: $200–$500

- Firearms: $2,500

- Silverware/Goldware: $2,500

- Business Electronics: $2,500

👉 High-value items require scheduled personal property coverage.

WHEN YOU NEED ADDITIONAL STORAGE INSURANCE

You should buy extra coverage if:

- Your items exceed your limit

- You live in a $1,000-cap state

- You are storing vehicles

- The storage facility requires insurance

Cost of Additional Storage Insurance

- Facility insurance: $15–$30/month (up to $10,000)

Third-party options may include:

- $0 deductible

- Coverage up to $75,000

- Replacement cost coverage

- Rodent damage protection

- Vehicle storage coverage

HOW TO FILE CLAIM FOR STORAGE UNIT LOSS

Step 1: Document Everything

Take photos and videos before moving items.

Step 2: File Police Report (if theft)

Required for claims.

Step 3: Contact Insurance Company

Report immediately.

Step 4: Provide Documentation

Inventory, receipts, proof of rental.

Step 5: Get Estimates

Repair or replacement quotes.

Step 6: Work with Adjuster

Inspection or additional review.

Step 7: Receive Payment

Example: $5,000 claim – $500 deductible = $4,500 payout.

DOCUMENTATION TIPS FOR STORAGE UNITS

- Take photos and videos

- Save receipts

- Create inventory list

- Record serial numbers

- Store documents offsite

- Update regularly

RENTERS INSURANCE VS STORAGE FACILITY INSURANCE

| Feature | Renters Insurance | Storage Facility Insurance |

|---|---|---|

| Coverage Limit | 10% or $1,000 | Up to $75,000 |

| Deductible | $500–$1,000 | $0 available |

| Covered Perils | Standard | Broader |

| Flood Coverage | No | No |

| Cost | Included | $15–$30/month |

| Convenience | One policy | Separate |

FREQUENTLY ASKED QUESTIONS

Does renters insurance cover storage units in another state?

Yes, coverage applies anywhere in the U.S.

Does renters insurance cover storage units during a move?

Yes, but transit coverage may differ.

Is storage unit insurance required by law?

No, but facilities often require it.

Does renters insurance cover climate-controlled units?

Yes, coverage is the same.

What about basement storage in my building?

Covered without the 10% limit.

Does storage coverage affect premiums?

No, but claims might.

Can I increase storage unit coverage?

Usually no, except indirectly via higher policy limits.

BOTTOM LINE

Renters insurance provides basic protection for storage unit belongings, but coverage is limited to 10% of your policy or $1,000.

For short-term storage, this is usually enough. For high-value or long-term storage, you should purchase additional insurance.

👉 Before renting a unit, calculate your stored property value. If it exceeds your limit, buy extra coverage and document everything to avoid claim issues.

Renters Insurance quote

Related Posts

Get a Right Insurance For You

SHARE THIS ARTICLE

We will compare quotes from trusted carriers for you and provide you with the best offer.

Whatever your needs, give us a call, have you been told you can’t insure your risk, been turned down, or simply unhappy with your current insurance? Since 1995 we’ve been providing coverage to our customers, and helping people across United States.

Note: This article is for informational purposes only and does not constitute professional advice. Always consult with a qualified insurance advisor before making any decisions regarding insurance coverage.