Does Renters Insurance Cover Storage Units?

We will search the top carriers for you for the best offer.

Does Renters Insurance Cover Storage Units? A Detailed Guide

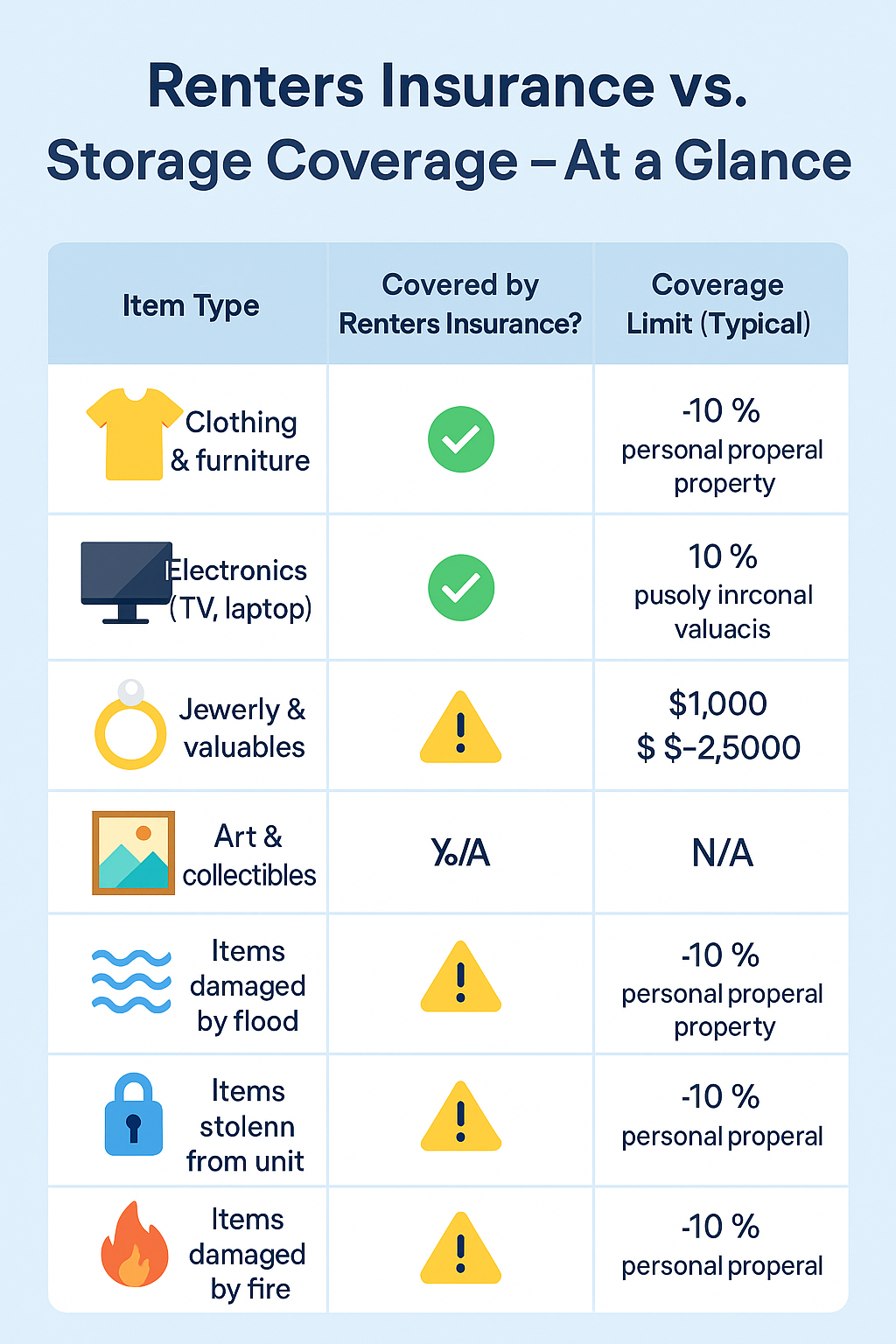

Yes, renters insurance usually covers items stored in a storage unit. Most policies include off-premises coverage, meaning your personal belongings are protected even when they are not in your apartment. However, coverage is typically limited to about 10% of your personal property limit and only applies to specific covered events.

Quick Answer

Renters insurance often covers belongings in storage units

Coverage typically equals about 10% of your personal property limit

Theft, fire, and vandalism are usually covered

Flooding, mold, and pests are usually excluded

High-value items may have additional sub-limits

How Renters Insurance Covers Storage Units

Most renters insurance policies include off-premises personal property coverage. This means your belongings can still be protected when stored outside your home, including in a storage facility.

However, the protection is typically lower than coverage inside your home.

Example scenario:

Personal property coverage: $40,000

Storage unit coverage (10% rule): $4,000

If items worth $6,000 are stolen from your storage unit, your policy may only reimburse $4,000 minus your deductible.

What Renters Insurance Typically Covers in Storage Units

Your belongings may be protected if they are damaged or stolen due to specific covered risks (called perils).

Common covered situations include:

Theft or burglary

Fire or smoke damage

Vandalism

Lightning strikes

Windstorms or hail

Sudden water damage from burst pipes

Covered items usually include:

Furniture

Clothing

Electronics

Appliances

Household goods

When Coverage Applies

Your renters insurance may pay for storage unit losses when:

Items are damaged by a covered peril

The belongings belong to you or household members

The claim amount falls within off-premises coverage limits

You pay the deductible required by your policy

Example:

You store furniture in a storage facility and a fire destroys the building. If your belongings were insured under your renters policy, the insurer may reimburse you up to the off-premises coverage limit.

When Coverage May Be Denied

Insurance companies may deny claims in these situations:

Damage caused by flooding

Loss due to mold, pests, or mildew

Normal wear and tear

Business inventory stored in the unit

Property belonging to someone else

Loss exceeding policy limits

Vehicles, aircraft, and animals are also typically excluded from renters insurance policies.

Special Limits for Valuable Items

Even if your policy covers storage units, certain high-value items have strict sub-limits.

Examples may include:

Jewelry

Cash

Collectibles

Fine art

Firearms

Silverware

For example, a policy might limit jewelry coverage to $1,500, even if your overall coverage is much higher.

To fully protect expensive items, you may need to schedule them individually or add extra coverage.

What to Do If Your Storage Items Are Worth More

If your storage unit contains valuable belongings, consider these options:

Increase your personal property coverage limit

Add an off-premises coverage endorsement

Purchase storage unit insurance from the facility

Schedule high-value items separately

Many storage facilities offer optional insurance policies specifically designed for stored property.

FAQ

Does renters insurance cover theft from a storage unit?

Yes. Theft is typically a covered peril, meaning your insurer may reimburse stolen items if they fall within your coverage limits.

Are storage units fully covered by renters insurance?

No. Most policies limit storage coverage to about 10% of your personal property limit, so protection is usually reduced compared to items in your home.

Does renters insurance cover water damage in storage units?

Sometimes. Sudden water damage (like a burst pipe) may be covered, but flood damage is usually excluded.

Are electronics covered in storage units?

Yes, but coverage may be limited and subject to the off-premises coverage cap.

Should I buy insurance from the storage facility?

It may be helpful if your belongings exceed the off-premises coverage limit of your renters policy.

Does renters insurance cover damage caused by pests in storage?

No. Damage caused by rodents, insects, or pests is generally excluded from standard policies.

Final Thoughts

Renters insurance can provide protection for items stored in a storage unit, but the coverage is usually limited and subject to exclusions. Most policies only cover about 10% of your personal property limit for belongings stored off-site.

If you plan to store valuable furniture, electronics, or collectibles, reviewing your policy limits or purchasing additional coverage can help prevent costly coverage gaps.

Get the Right Renters Insurance Coverage

Are you facing potential liability or want to ensure your property is protected against unexpected losses? Fill out the form below to get expert guidance and a tailored insurance solution from our network of carriers.

With 30 years of professional experience, we compare nearly 100 insurance companies to find the best coverage at the best price.

Start now and see your options instantly.

Get your personalized quote today. It’s fast, secure, and tailored to you.

Renters Insurance quote

Related Posts

Get a Right Insurance For You

SHARE THIS ARTICLE

We will compare quotes from trusted carriers for you and provide you with the best offer.

Whatever your needs, give us a call, have you been told you can’t insure your risk, been turned down, or simply unhappy with your current insurance? Since 1995 we’ve been providing coverage to our customers, and helping people across United States.

Note: This article is for informational purposes only and does not constitute professional advice. Always consult with a qualified insurance advisor before making any decisions regarding insurance coverage.